As early-stage investors, we’ve been hearing for years an undeniably loud chorus of founders lamenting that many venture capital funds, particularly top-tier ones, won’t even take a meeting with them because they lack a Stanford or Harvard University diploma. We also heard over and over again that founders who lacked education pedigree saw highly discounted valuations. In some cases, the anecdotal evidence was stark.

I remember the case of two telehealth startups that our team reviewed over the span of a few months. One was led by a Harvard-educated founder with an idea. The other was led by founders from mid-tier American universities and were already doing over $20 thousand in monthly revenue. We judged the two investments to be relatively equal on every other parameter, such as industry experience and team skill set. The first startup (led by Harvard alumni) had secured more than half their round at a $15 million valuation for their idea. The other startup, which had been raising longer, secured $150 thousand at a $6 million valuation. Once again, as far as we could tell, the latter was the stronger business, having removed product and customer risk to a large extent. The only difference we could see was what diplomas hung on the founders’ walls.

This brought up several questions for our team: Are other VC investors truly biased in favor of founders with educational pedigree? Are we missing something bigger, deeper, or more nuanced? Is there a market asymmetry here that could lead to outsized returns? These are questions of obvious pertinence to us as fund managers and to startup founders, who often feel they are fighting a losing battle.

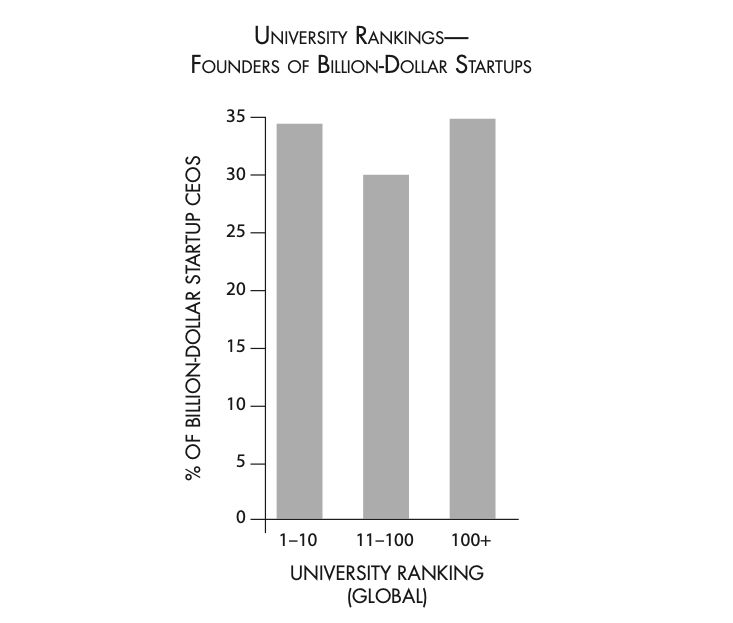

The first breakthrough in unraveling these questions came in the form of an excellent book by Ali Tamaseb, Super Founders: What Data Reveals About Billion-Dollar Startups. Mr. Tamaseb investigated 30,000 data points to better understand what factors might lead to billion-dollar startups. One of the dimensions that he studied was the founders’ or CEOs’ educational pedigree. Interestingly, Tamaseb found that alumni from universities that were not even in the top 100-ranked universities globally built just as many billion-dollar startups as those who graduated from a top-10 university. This seemed to align with the success rates we’ve been seeing among the startups that we’ve tracked, but it failed to answer the fundamental question: Does a pedigree bias truly exist, especially among top-tier funds? After all, if 35% of investment is going to startups led by founders of top-ten universities, who go on to build 35% of unicorn companies, that seems like a commensurate allocation.

To better understand this problem (or opportunity) our team devised a small quasi-scientific study to measure how often leading venture capital firms invest in startups led by alumni of top universities. We chose to look at top-tier firms because they have earned their distinction through inspiring track records, and because founders often claim that these firms place the greatest emphasis on the caliber of founders’ alma maters. What we found truly surprised us, and while answering some questions, the result of our study generated many more puzzles.

Methodology

Our study examined investments made between 2018 and 2023 by the leading ten U.S. venture capital firms as ranked by Deal Room, a research-backed mergers and acquisitions platform. The firms included in this study are listed in the table below:

Top 10 Leading Venture Capital Firms

Source: Deal Room’s 15 Top Venture Capital Firms in the World

We looked at a total of 843 investments made by these top firms at the seed stage during the five-year period, as reported on the investment research platform, Crunchbase Pro. We chose to look at the seed stage because that was the data set more relevant to us as a pre-seed and seed firm, but also it’s the main on-ramp for most startups to venture capital. Our team researched the founding team and their educational backgrounds using publicly available data and cross-referenced these with prestigious schools both globally and in the United States.

The schools we included in this study were chosen based on notable ranking lists, specifically the 2023 US News & World Report National Rankings and the 2023 Times Higher Education's World University Rankings. Beyond the top 20 listed on each of these rankings, we further analyzed the data against the most elite schools in the United States: Ivy League universities, plus Stanford University, Massachusetts Institute of Technology, and Duke University (sometimes referred to as “Ivy League Plus” universities).

Findings

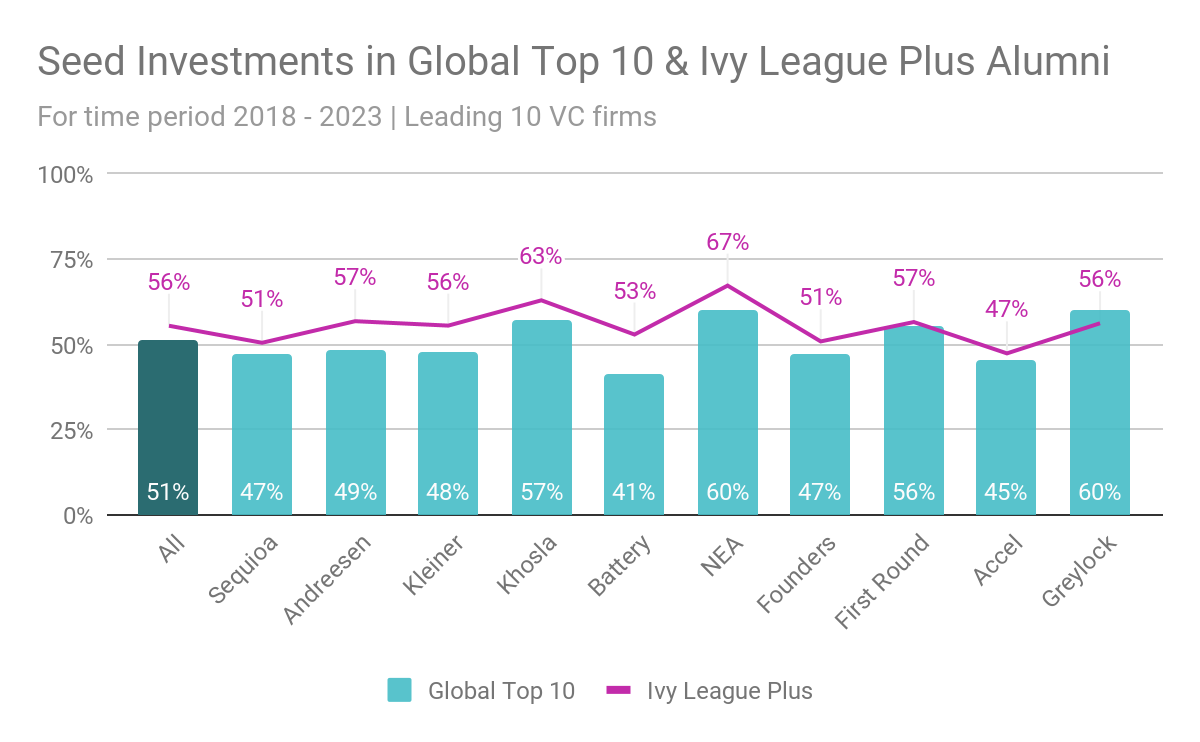

At a summary statistics level, we found that the top ten firms in our study invested more frequently in seed-stage startups led by founders from top-10 universities, by a margin of 51% to 49%. Some funds such as NEA (60%), Greylock (60%), and Khosla Ventures (57%) are almost twice as likely to invest in seed-stage startups led by founders from top-ten universities than led by alumni of any other university.

This is relevant because, according to Ali Tamaseb’s research mentioned above, only 35% of unicorn companies were led by alumni of top-10 universities. This would suggest that some firms are over-indexing by nearly 2:1 in alumni of top-10 universities at the seed stage.

Those firms that seem to be partial to founders with greater educational diversity are Battery Ventures (41%), Accel (45%), Sequoia (47%), and Founders Fund (47%).

NEA shows the greatest preference for Ivy League Plus alumni with 67% of their investments going to seed-stage startups led by alumni of those schools, with Khosla following closely behind at 63%.

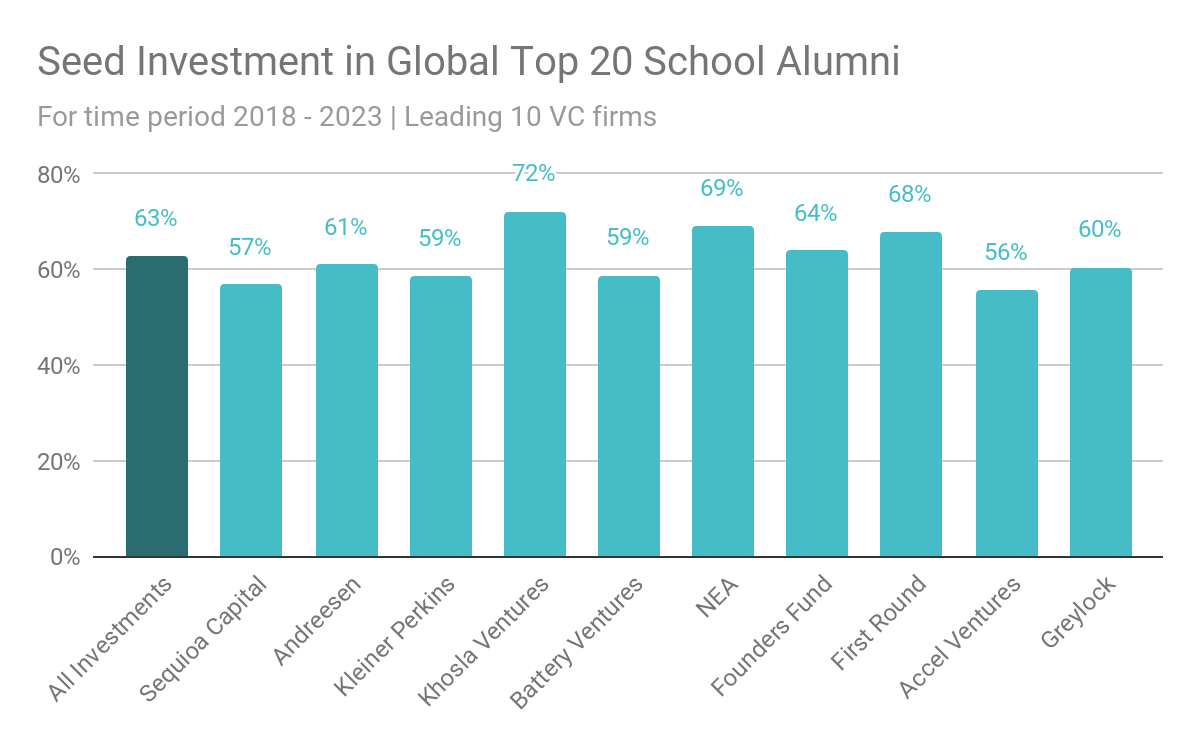

When we zoom out a bit to the top 20 universities globally, an even stronger preference seems to appear. Across all ten funds, the average investment rate in alumni of top-20 universities globally becomes 63%, with some funds like Khosla (72%), NEA (69%), and First Round (68%) having roughly two-thirds of their investments going to alumni of those schools.

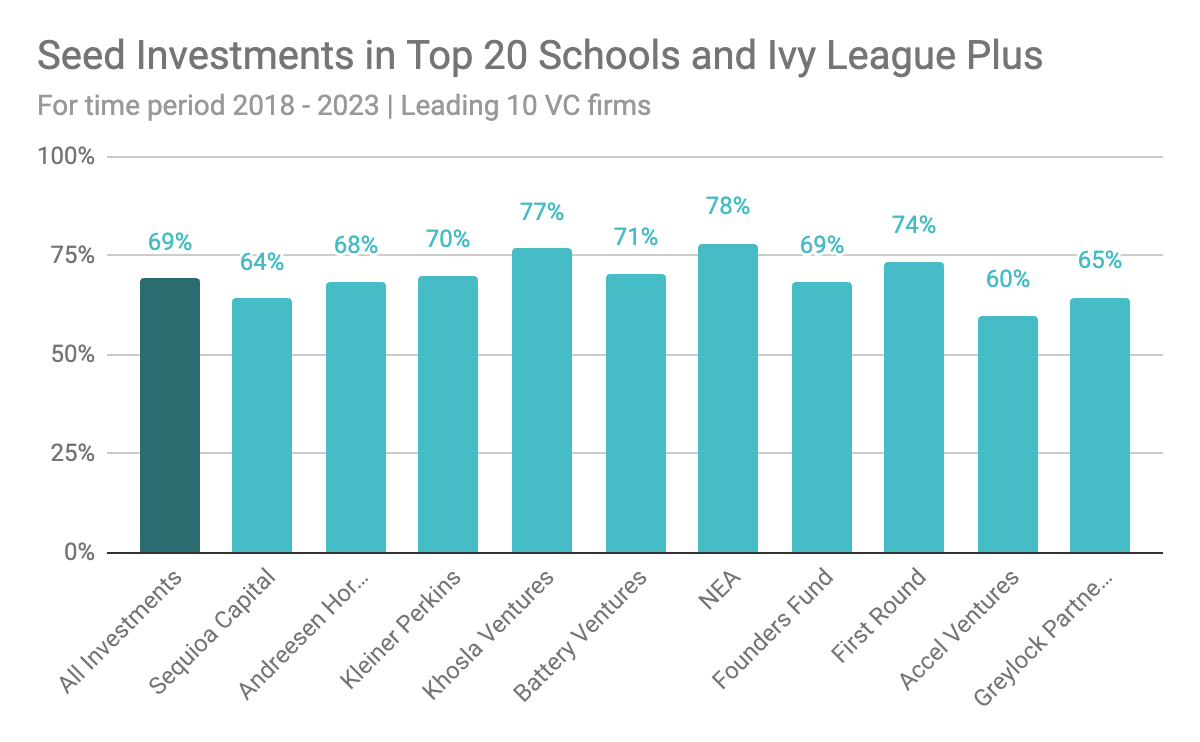

Looking at this disparity with a wider aperture of all markers of pedigree — across the top 20 schools in the U.S. and globally, and Ivy League plus — we see that 69% of the investments went to this elite group of alumni. In this case, half of these leading firms exceed 70% allocated to this elite founder group, namely NEA (78%), Khosla Ventures (77%), First Round Capital (74%), Battery Ventures (71%), and Kleiner Perkins (70%).

Discussion

Although this was a fairly simple study, our team did find evidence that top venture capital funds seem partial to seed-stage companies led by alumni from elite universities. Many factors go into investment decisions such as time to exit, potential exit size, risk, etc., but if we are optimizing for exit size, looking at how these proportions relate to the proportion of billion-dollar companies being created might expose an opportunity. Indeed, if only 35% of unicorn companies are led by alumni of top-10 universities but some of the firms in our study make as many as 60% of their investments in alumni of those same universities, this disparity in proportions might suggest an opportunity for outsized investment returns. Or as investors like to say, “alpha.”

Does pedigree bias lead to better investment outcomes?

The first and obvious question is whether favoring founders from prestigious universities leads to better investment outcomes. Obviously, the firms in our study are at the apogee of the venture capital industry because of their long and meritorious history. The question is not whether these firms, or any other venture capital firms, did something wrong, but rather could they have done even better by investing a greater proportion of their capital in teams without prestigious degrees? Or maybe they would have achieved lower returns had they not followed their chosen allocation strategy.

This question is a lot harder to answer and requires much more robust data and statistical analysis than our small team was able to accomplish. Indeed, this point alone can probably keep a small army of business and economics researchers busy for some time to come.

Having said that, if alumni from universities not ranked in the top 100 globally are just as likely to create unicorn companies as Super Founders indicates, higher returns should be possible from a contrarian investment strategy of investing in non-pedigree founders. Particularly at the earlier stages when funds’ returns are driven by outlier outcomes, if the probability of a founder from a top-ten university building a billion-dollar company is essentially the same as that of a founder from a lesser-known school, several conditions could theoretically lead to an economically favorable arbitrage situation:

- Startups that are led by founders from elite universities raise capital at a premium;

- It’s easier to identify equally promising startups led by non-pedigree founders;

- It’s easier to participate in rounds of startups led by non-pedigree founders.

Certainly, at least two of the above conditions do not seem unreasonable.

More broadly, there is impressively scant research drawing a link between founders' educational attainment and entrepreneurial outcomes. Several studies show no statistically significant relation between the two. For example, a 2012 study by Gerard Groenewegen and Frank Langen titled “Critical Success Factors of the Survival of Start-Ups with a Radical Innovation” didn’t even find a direct relationship between a college degree and entrepreneurial success. Similarly, a 2006 study by Amason et al. found no correlation between startup performance and the education of their management team. This might not be terribly surprising when you consider super founders like Michael Dell, who dropped out of the University of Texas, and Melanie Perkins, who attended the University of Western Australia (ranked #83 in Best Global Universities by US News).

Does pedigree bias exist in later stages of investment?

Perhaps a more accessible question to answer is whether this pedigree bias exists for top-tier VC firms during later (growth and expansion) rounds of financing. One of the common refrains that we hear from other investors and limited partners is that it’s not wise to invest in startups led by non-pedigree founders because it will be more difficult for them to raise subsequent rounds of funding. If this is true, then we’d expect to see these ratios hold steady into later rounds, or perhaps even become more skewed.

Having performed an extensive literature review, our team found only one study that seemed to address this very question: a 2019 paper by Snehal Shetty and Ranjany Sundaram titled “Funding acquisition drivers for new venture firms: Diminishing value of human capital signals in early rounds of funding” which looked at the funding rounds of 156 startups in India established between January 1, 2010, and December 31, 2015. In their study, the authors did indeed find a correlation between the amount of capital raised in the firms’ first, second, and third rounds of funding and the founders’ educational pedigree. However, it’s unclear to what extent their results are externally valid beyond the scope of their study.

How does pedigree bias vary across the VC industry?

According to Pitchbook, over 48,000 venture capital firms are operating worldwide. It goes without saying that the venture capital universe is as varied as one dares to imagine. Firms range in size from one general partner to hundreds of staff. They vary in their industry, geography, and stage focuses. They are different in hundreds of other ways too.

It would be fascinating to see how different kinds of firms favor or disfavor founders from top universities, but doing a study of tens of thousands of firms is far beyond the bounds of this study. Challenge proposed.

Other than potential outcomes, what else is pedigree bias causing us to miss?

While the universities in our study top various prestige rankings, they are among the worst performers when it comes to representation of economic or ethnic diversity. Why might this be a problem?

I think most of us agree that the most successful innovators solve problems that they know intimately well. If the venture capital industry underinvests in founders who didn’t attend prestigious universities, could we be missing out on innovations addressing the needs of non-wealthy or multiethnic consumers?

Where do we go from here?

Why is pedigree bias relevant in the VC industry and to the broader economy? Most would probably say that it’s worth our attention if it’s causing an inefficient allocation of venture capital to economically and socially impactful enterprises. That’s really the big question: Could we as an industry be doing even better by investing in founders from more diverse educational backgrounds?

References

Amason, A. C., Shrader, R.C., & Tompson, G. H. (2006). Newness and novelty: Relating top management team composition to new venture performance. Journal of Business Venturing, 21(1), 125-148.

Groenewegen, Gerard & Langen, Frank. (2012). Critical Success Factors of the Survival of Start-Ups with a Radical Innovation. Journal of Applied Economics and Business Research. 2. 155-171.

Snehal Shetty and Ranjany Sundaram (2019). Funding acquisition drivers for new venture firms: Diminishing value of human capital signals in early rounds of funding. Problems and Perspectives in Management, 17(1), 78-94.

About Beta Boom

Beta Boom is pre-seed and seed fund investing in founders who defy the mainstream.

BETA BOOM BACKS ORIGINALS

Investing at the pre-seed and seed stages in founders who defy the mainstream.

.png)

.png)